While HFLA of Northeast Ohio is here to provide interest-free loans to those who need them, the ultimate goal is to not need one. How? Meet your new best friend – a Savings Plan.

Ideally, a savings account or emergency fund can give you the cash you need in times of crisis without relying on loans or cash advances.

Unfortunately, we are all currently stuck smack in the middle of a global health crisis. A crisis that is having a major impact not only on our daily lives and health, but especially on our income and personal savings. Fortunately, many of us will be receiving a tax refund that can give our finances a boost. While cash during this crisis may feel like the answer to all your problems right now, it is important to use this money wisely and to think long-term. This can help you take effective steps towards a long-term savings plan to get you and your family through this pandemic and find financial security in the future.

What is an Emergency Fund?

The rule of thumb for an “Emergency Fund” is 3 months worth of living expenses in your savings account. The reality however, is that many Americans struggle to come up with $1,000 in an emergency. We at HFLA do feel that it is crucial to develop an emergency fund however, it doesn’t have to happen overnight. A slow and steady strategy will allow you to gradually and reasonably work up to your savings goals.

Observing prudent savings strategies now will make a world of difference once we all come out the other side of the COVID-19 Pandemic.

Take Advantage of Your Tax Refund in 2 Ways

Luckily for many of us, income tax refunds can provide some much needed “bonus” cash that can be used to stabilize your finances.

1. Add one month of living expenses to your savings

You just worked out your monthly expenses, so if you can, add that total to your savings now with your tax refund!

Remember to include: rent/mortgage, food, utilities, car note, minimum credit card payments, and insurance. Can you take this amount out of your tax refund? If yes, put that into your savings IMMEDIATELY! If not, try to put a portion of that into your savings and strive to save the rest up throughout the year.

2. Catch up on collections or due balances

Review your credit report on AnnualCreditReport.com to see if you are behind on any collections or any accounts.

Use your tax refund to give your credit a boost and get caught up on things that are too big to tackle all at once. Consider speaking to a financial coach or financial counselor to help you with clear goals on what debts to tackle first.

3 Tips to Start Saving Without Breaking the Bank!

Some simple ways to start reaching your financial goals, even on a tight budget.

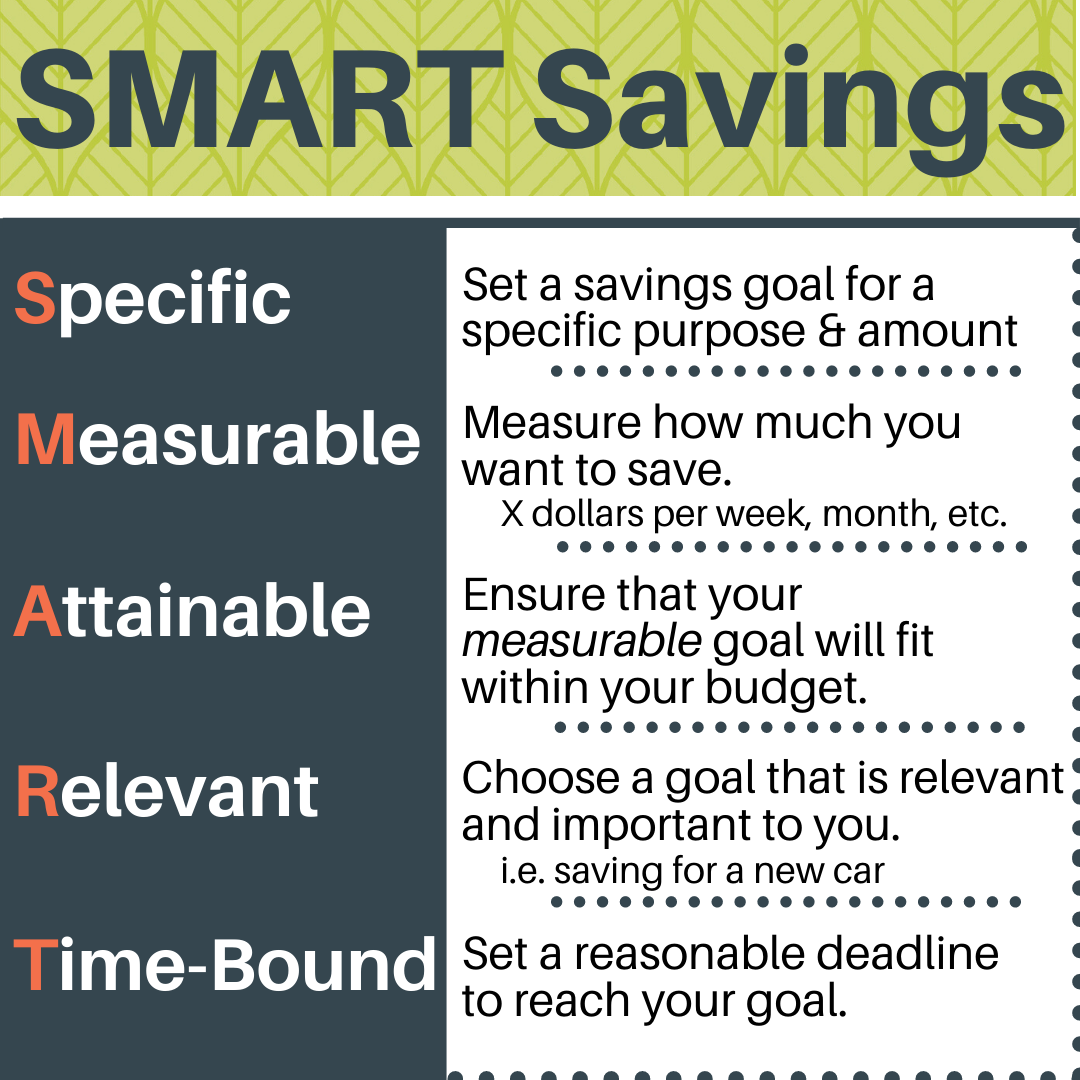

1. Make a SMART plan for your savings goal

Let’s say you want to save up one month’s living expenses, equaling $500, in one year.

Your specific goal is to contribute one month’s living expenses to savings measured to be $500 total. Your regularly measured goal equals $42 a month over 12 months. You check, “Is this goal attainable with my current income and expenses?” If yes, stick with it! If no, lower the measurable goal to something that fits within your budget. You ask, “Is this goal relevant, will it help me in the long run?” Yes! You will eventually have one month of living expenses that could be relevant during an emergency! You set a goal date of 12 months to keep your goal time-bound.

Once you’ve achieved one SMART goal, make another! Check out this worksheet from Consumerfinance.gov and create your own.

2. Set up direct deposit and “pay yourself” first

If you haven’t already, set up direct deposit to get your paychecks into your bank account quickly and safely.

Every time you receive a paycheck, “pay yourself” first! Take a predetermined amount from your paycheck and deposit it into your savings account before spending anything! By contributing a small portion of every paycheck into your savings account, you are growing your savings fund at least once a month without having any time to to spend it. Some banks also offer automatic savings that directly takes a designated amount of your paycheck each time. Even $5 a paycheck can go a long way when you stick with it!

3. Become a “Brown-Bagger”

Making the change from buying to packing lunch is definitely a lifestyle commitment, but one that can save you thousands of dollars annually.

One cup of coffee a week can be anywhere from $2-$5 dollars. That alone adds up to at least $100 a year! Getting takeout can be inexpensive, but still at least $5 a day. Make your coffee at home, plan your meals the day before, and put that money back in the bank! Every time you feel the urge to buy food or coffee instead of making it yourself, total up what you are about to spend and put that money into your savings instead. You’ll be amazed to see how much you would have spent!

And most importantly, don’t touch your savings account!

Keep your hands out of your savings account as much as you can. Treat it like it is money only to be spent in an emergency. Schedule dates where you check on it’s growth. You’ll be surprised with how much you’ve put away in such a short time by keeping your hands off and eyes out!

About HFLA of Northeast Ohio

HFLA of Northeast Ohio was founded in 1904 with $501 donated by Charles Ettinger, Morris Black, and their friends to help European refugees settle and begin productive lives in this country. They believed – as we do now – that if you give someone a chance to succeed, they will pay it back and we can continue this transformative cycle. The same principle guides the organization today. By providing interest-free loans to individuals, families, and small businesses in the Northeast Ohio area, we are able to help people help themselves. The association has drastically increased its lending capital in the past few years from individual gifts, bequests, endowments, foundation grants, memorials and honorariums and is now operating with a loan fund of over $1 million. HFLA is a 501(c)3 non-profit organization. Learn more about HFLA.

Get involved and stay up to date by subscribing to our quarterly newsletter or following us on social media.