Unbanked and Underserved: The Importance of a Bank Account

Nationally, more people than ever are opening bank accounts. Opening and maintaining a bank account can be one of the most effective ways to achieve your financial goals, including increasing your credit score, buying a house, or just finding financial security. In 2023, the US’s unbanked rate dropped to 4.2%-- the lowest level since 2009. Northeast Ohio, however, is seeing a different trend. The unbanked rate in NEO increased from 2.0% in 2021 to 5.4% in 2023–an increase of over 3%!

There are a variety of reasons why people avoid mainstream financial institutions:

- Lack of trust: Many groups have been victims of racist and exclusionary practices by the mainstream financial industry that have systematically left them out of the system.

- Minimum Deposit: Until recently, most banks required a minimum amount to even open an account and maintain the account, making them inaccessible for many people with inconsistent income.

- Fees: With inconsistent income, many people face high overdraft and/or administrative fees, making traditional banking too costly.

Groups that are typically left out of traditional banking tend to be “lower-income, less-educated, Black, Hispanic, disabled, and single-parent households.” Households of color are five times more likely to be un- or under-banked compared to white households.

Those unable or unwilling to participate in the mainstream financial industry have few other options. For most, the only option is to rely on predatory services that require high fees and implement exorbitant interest rates, forcing people to pay up to 5% of their income to access their own money. This could add up to over $40,000 over one’s lifetime. These predatory lenders send people into a cycle of debt that becomes untenable and leads people further into financial instability. Even those who may have a bank account can be considered “underbanked” when they still rely on nonbank financial services, such as check cashing services or pawn shops, and therefore are still vulnerable to exploitative practices.

This is not inevitable. Bank accounts provide many opportunities in the modern economy, like establishing and building credit, avoiding fees to access their money, and growing wealth.

The Consumer Financial Protection Bureau under the Biden Administration has recently ruled to crack down on bank overdraft fees, offering banks the option to either have a flat $5 fee, cap the fee to cover costs and losses, or “charge any fee but disclose the terms of the overdraft loan they extend to customers the same way they would for those of any other loan.” This new rule can save consumers $5 billion, or roughly $225 per household. Many banks have stepped up to the challenge of making mainstream banking more accessible. Working with the Bank On National Advisory Board and Coalitions across the country, like the ones in Cleveland and Summit County, banks have lowered the barriers to banking. This includes limiting fees, removing minimum balance requirements, and working with community partners to connect people to accounts.

HFLA of Northeast Ohio can provide a third option.

HFLA has offered 0% interest loans for 120 years. Rather than continuing to spiral into a perpetual cycle of uncertainty, our loans give people the chance to stabilize their financial situation and start on the path of rebuilding. Our applicants are individuals who often get turned away from traditional banks. They are seeking help to address a need like a required home repair, medical bills, or to get out from predatory loans. We ensure that our loans are accessible, affordable, fast, and fair. Our loans are not “easier” to qualify for, but we work to remove barriers to help people get much needed capital. People are so much more than a 3-digit credit score. We try to understand the whole picture and prioritize repayment history and budgeting plans when considering their application.

There are still some barriers. All of our loans require a cosigner or guarantor. As a nonprofit, we rely on our loans being paid back to continue our work. Co-signers and guarantors provide a level of security to ensure that the loan is paid back in full.

Our staff will work with an individual through the complete repayment of the loan. Successful repayment is just as important to us as their loan payments go back into our revolving loan fund to help fund someone else’s loan, continuing the cycle. Our hope is that you come to HFLA for your first loan and through our support (and credit reporting) you will be able to access the mainstream financial system for your second loan.

With unbanked rates increasing in the Northeast Ohio area, support is needed now more than ever. Since 1904 HFLA has created financial opportunities for its community. If you want to support HFLA’s mission, you can donate here to assist with operational costs to keep our organization going. If you know someone who might benefit from an HFLA loan, please visit us at interestfree.org or contact us at team@interestfree.org.

To learn more about this topic, take a look at the Federal Reserve Bank of Cleveland’s FedTalk: “A Continued Discussion on Financial and Payments Inclusion”.

Debt Exchange Loan Program

Debt Exchange Loan Program

August 5, 2021 | Program Director, Brady Gasser

Since 1904, the HFLA of Northeast Ohio has provided interest-free loans for individuals with needs that cannot be met by the mainstream lending industry. Our creative approach to relationship lending has allowed us to continuously make sense of our changing world and adapt our offerings accordingly. Most recently, we have made some exciting changes to address needs for debt refinancing and consolidation.

Many in our community find themselves with punishing or unsustainable debt obligations. Personal loans from non-traditional institutions can be accessed online, but with absurdly high interest rates.

This would be the most obvious example. However, even some standard rates and practices, like those found with private student lenders are more than suboptimal. An individual may have felt like they were forced into taking on bad debt because they did not see another path out of their predicament; or they could regret past decisions because they were uninformed about the true ramifications at the time they took on the debt. Learning the hard way is one thing, but some debts are so egregious that no amount of struggle by the individual can meaningfully correct a wrong move.

Our Debt Exchange Loan Program is designed to help individuals strengthen their financial position by trading in overly burdensome interest-bearing debts for an interest-free loan.

This loan can be used to address up to $10k in debts like private student loans (not issued from the government), credit cards, “payday” and other personal loans, and collections accounts. The total amount of such debt held by Northeast Ohioans is much more than HFLA will be able to exchange. As a small non-profit, we are only able to help those who are truly in need. Therefore, good candidates will be able to clearly express a strong need to exchange the debt, have a specific personal financial plan, and show a commitment to the betterment of their financial wellbeing. Working with a partnering financial coach may be a prerequisite to qualify based on an assessment by HFLA staff.

Once the debt is exchanged, individuals will see many immediate and long term benefits that can multiply. First, once the debt is paid off with the original creditor, it will stop accruing interest, which will save the individual money in the long term. Many individuals will see a lower monthly repayment with HFLA, which can free up money in their monthly budget to put towards necessities, other debts, or savings. Whether it is because of a new lower monthly payment or gaining the ability to pay off debt more quickly, some will see an improvement in their debt to income ratio, which can help them access a larger, prime loan that they may need (like a home equity line of credit). For those that exchanged revolving debt (credit cards), they will see an immediate improvement in their credit score as their credit utilization will decrease dramatically. Additionally, HFLA does not necessarily require that revolving accounts that are paid off be closed, so this increase in credit score will last as long as the accounts are kept at a zero dollar balance. Paying off collections accounts can get collections agencies off of your back and can help increase your credit score for some scoring models.

Please call or email our program department to find out how you may be able to qualify and benefit from the Debt Exchange Loan Program. Personal guarantors (outside of a borrower’s household) are required for any loan applicant.

216-378-9042 menu option #1

Savings Strategies for a Tight Budget

While HFLA of Northeast Ohio is here to provide interest-free loans to those who need them, the ultimate goal is to not need one. How? Meet your new best friend – a Savings Plan.

Ideally, a savings account or emergency fund can give you the cash you need in times of crisis without relying on loans or cash advances.

Unfortunately, we are all currently stuck smack in the middle of a global health crisis. A crisis that is having a major impact not only on our daily lives and health, but especially on our income and personal savings. Fortunately, many of us will be receiving a tax refund that can give our finances a boost. While cash during this crisis may feel like the answer to all your problems right now, it is important to use this money wisely and to think long-term. This can help you take effective steps towards a long-term savings plan to get you and your family through this pandemic and find financial security in the future.

What is an Emergency Fund?

The rule of thumb for an “Emergency Fund” is 3 months worth of living expenses in your savings account. The reality however, is that many Americans struggle to come up with $1,000 in an emergency. We at HFLA do feel that it is crucial to develop an emergency fund however, it doesn’t have to happen overnight. A slow and steady strategy will allow you to gradually and reasonably work up to your savings goals.

Observing prudent savings strategies now will make a world of difference once we all come out the other side of the COVID-19 Pandemic.

Take Advantage of Your Tax Refund in 2 Ways

Luckily for many of us, income tax refunds can provide some much needed “bonus” cash that can be used to stabilize your finances.

1. Add one month of living expenses to your savings

You just worked out your monthly expenses, so if you can, add that total to your savings now with your tax refund!

Remember to include: rent/mortgage, food, utilities, car note, minimum credit card payments, and insurance. Can you take this amount out of your tax refund? If yes, put that into your savings IMMEDIATELY! If not, try to put a portion of that into your savings and strive to save the rest up throughout the year.

2. Catch up on collections or due balances

Review your credit report on AnnualCreditReport.com to see if you are behind on any collections or any accounts.

Use your tax refund to give your credit a boost and get caught up on things that are too big to tackle all at once. Consider speaking to a financial coach or financial counselor to help you with clear goals on what debts to tackle first.

3 Tips to Start Saving Without Breaking the Bank!

Some simple ways to start reaching your financial goals, even on a tight budget.

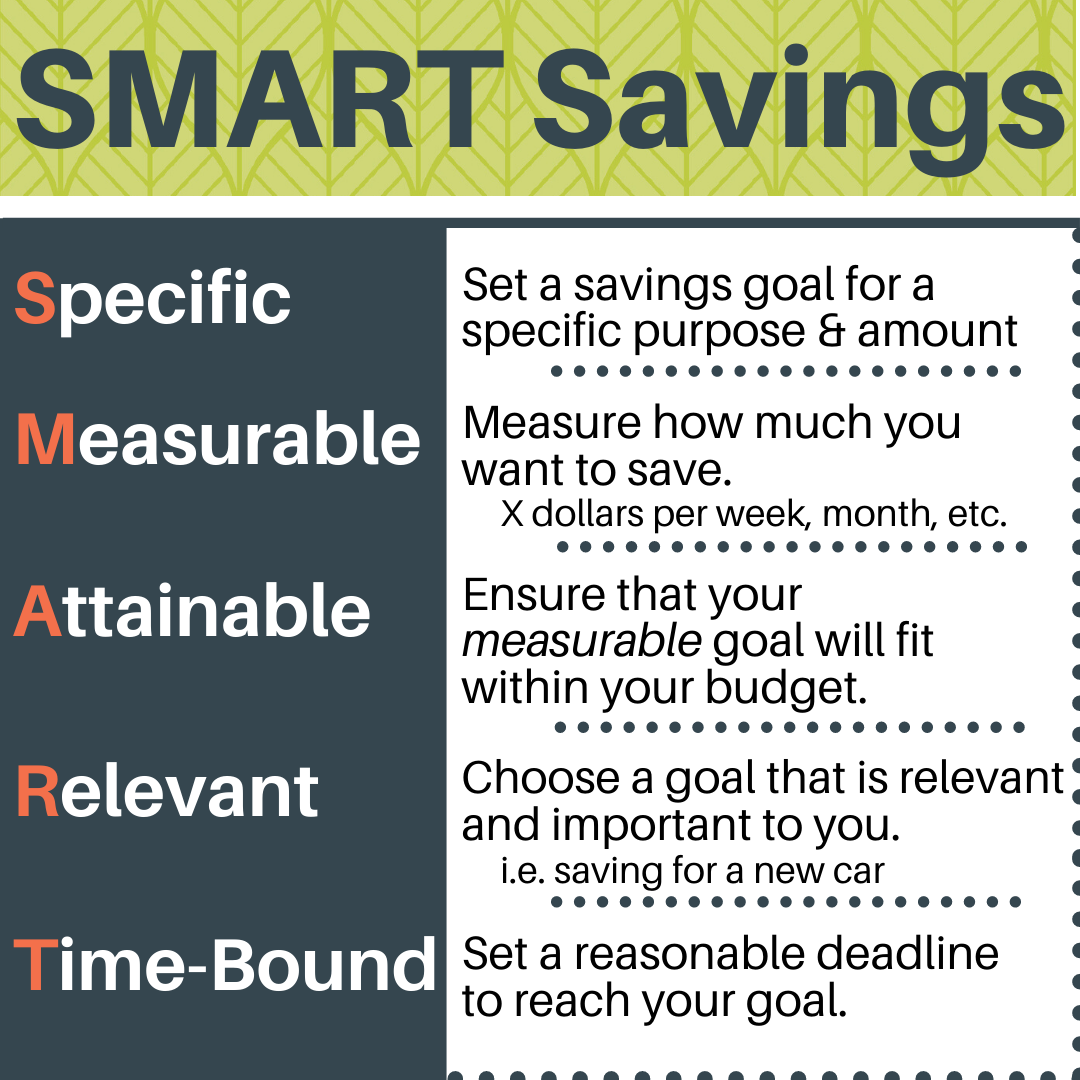

1. Make a SMART plan for your savings goal

Let’s say you want to save up one month’s living expenses, equaling $500, in one year.

Your specific goal is to contribute one month’s living expenses to savings measured to be $500 total. Your regularly measured goal equals $42 a month over 12 months. You check, “Is this goal attainable with my current income and expenses?” If yes, stick with it! If no, lower the measurable goal to something that fits within your budget. You ask, “Is this goal relevant, will it help me in the long run?” Yes! You will eventually have one month of living expenses that could be relevant during an emergency! You set a goal date of 12 months to keep your goal time-bound.

Once you’ve achieved one SMART goal, make another! Check out this worksheet from Consumerfinance.gov and create your own.

2. Set up direct deposit and “pay yourself” first

If you haven’t already, set up direct deposit to get your paychecks into your bank account quickly and safely.

Every time you receive a paycheck, “pay yourself” first! Take a predetermined amount from your paycheck and deposit it into your savings account before spending anything! By contributing a small portion of every paycheck into your savings account, you are growing your savings fund at least once a month without having any time to to spend it. Some banks also offer automatic savings that directly takes a designated amount of your paycheck each time. Even $5 a paycheck can go a long way when you stick with it!

3. Become a “Brown-Bagger”

Making the change from buying to packing lunch is definitely a lifestyle commitment, but one that can save you thousands of dollars annually.

One cup of coffee a week can be anywhere from $2-$5 dollars. That alone adds up to at least $100 a year! Getting takeout can be inexpensive, but still at least $5 a day. Make your coffee at home, plan your meals the day before, and put that money back in the bank! Every time you feel the urge to buy food or coffee instead of making it yourself, total up what you are about to spend and put that money into your savings instead. You’ll be amazed to see how much you would have spent!

And most importantly, don’t touch your savings account!

Keep your hands out of your savings account as much as you can. Treat it like it is money only to be spent in an emergency. Schedule dates where you check on it’s growth. You’ll be surprised with how much you’ve put away in such a short time by keeping your hands off and eyes out!

About HFLA of Northeast Ohio

HFLA of Northeast Ohio was founded in 1904 with $501 donated by Charles Ettinger, Morris Black, and their friends to help European refugees settle and begin productive lives in this country. They believed – as we do now – that if you give someone a chance to succeed, they will pay it back and we can continue this transformative cycle. The same principle guides the organization today. By providing interest-free loans to individuals, families, and small businesses in the Northeast Ohio area, we are able to help people help themselves. The association has drastically increased its lending capital in the past few years from individual gifts, bequests, endowments, foundation grants, memorials and honorariums and is now operating with a loan fund of over $1 million. HFLA is a 501(c)3 non-profit organization. Learn more about HFLA.

Get involved and stay up to date by subscribing to our quarterly newsletter or following us on social media.